LinearWorld

Investment Thesis

Impinj, Inc. (NASDAQ:PI) operates a platform for cloud connectivity worldwide. It consists of multiple product families that connect singular items wirelessly and deliver data to customer applications and businesses regarding the connected items. The platform consists of integrated circuits [ICS] and systems products. It serves various sectors, mainly; retail, healthcare, automotive, and supply and logistics, to mention but a few.

The company offers RAIN RFID innovative solutions to global businesses. It has gone further and expanded the capabilities of these chips, which has provided an opportunity for widening its array of solutions. There is also a strong demand for its products, resulting in an increase in its order backlog. These variables have taken part in its ongoing growth. PI has also seen an appreciation in its stock by 118.31% over the past year and recorded decent revenues in the MRQ. Additionally, its revenues and earnings are expected to grow in the future.

PI has recently invested by acquiring Voyantic, a market leader in test and measurement solutions. Following this acquisition, I am bullish on the stock due to its strong demand for its products and outlook.

Expanding Chips Capabilities

The company has already established its position as a tracking chip provider for effective inventory management and continues to experience growth. Currently, it has been broadening its chips' functionalities to services such as loss prevention, retail automated self-checkout, and anticounterfeiting.

Automated self-checkout and loss prevention

The Impinj Protected Mode is a cutting-edge capability in the Impinj M700 series tag chips. It increases the performance, flexibility, and privacy of RAIN RFID by controlling where and when tagged items are read and making tag data invisible to unauthorized readers. The automated self-checkout systems have enhanced the customers' buying experience, as they have the convenience of ringing up a basket of items immediately in one go.

With the Protected Mode feature, tags are turned off when purchases are made, and in case of a product return, they are turned back on. Additionally, it has enhanced the effectiveness of loss prevention by rendering purchased item tags invisible to RAIN RFID readers.

Anticounterfeiting

The Impinj Authenticity Solution Engine is an innovative solution that has enabled the verification of legitimate products through cryptographic authentication at every stage of the supply chain. This ensures product safety, prevents counterfeits, and secures the supply chain.

The retail sector is a primary market for the company since approximately 70% of RFID tracking chips are used by the industry, especially apparel, with RFID covering 25% of its market. Impinj is utilizing the above opportunities to continue building and driving its growth by increasing its range of innovative solutions.

Demand and Supply Interplay

PI has seen strong demand for its products; its data reading hardware and endpoint RFID tags. Historically, the company has recorded a 25% to 30% yearly demand growth for RAIN RFID. It has expressed its positive sentiment that the encouraging market reception seems to extend into the first six months of 2023, resulting in an increased order backlog.

Despite the strong demand, Impinj has been hindered by supply constraints. It has faced component and semiconductor shortages for its systems business and RAIN RFID tags. In the third quarter of the fiscal year 2022, the company mentioned that for the last six quarters, demand surpassed its production capacity by more than 50%, thus subduing its growth. This headwind persisted in its Q4, but there were early signs of easing. Currently, this supply bottleneck is easing up, and PI can deliver its offerings to the strong demand.

What do the Figures Say?

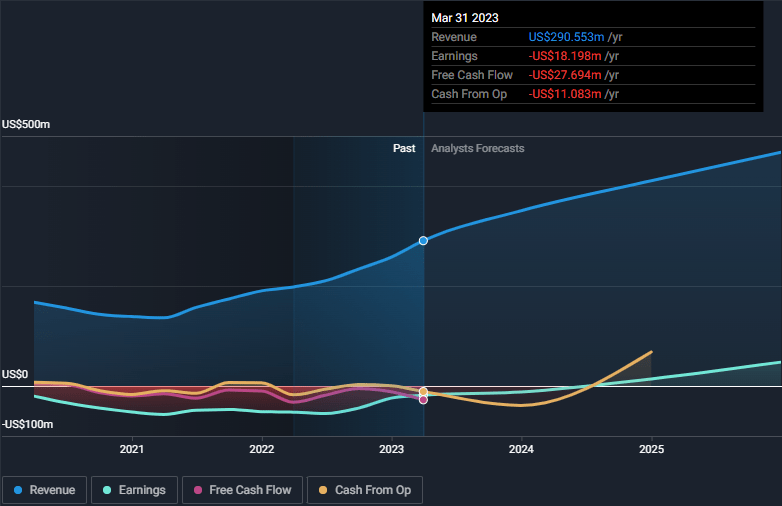

PI's stock has appreciated and is about 118.3% higher than this past year, which is quite alluring. Over the trailing twelve months, Impinj has not been profitable; therefore, there is a slim chance of observing a significant correlation between its EPS and stock price. Focusing on revenue is plausibly the next best shot. Companies that don't record profits are expected to generate positive revenue growth. With this, earnings can be easily projected.

In the first quarter of 2023, PI reported a 61% year-over-year revenue growth to $ 85.9 million, a 12% increase from the previous quarter. This report revealed a revenue surprise, exceeding the consensus by $ 2.3 million. The company has a CAGR [TTM] of 19.6% over the last five years, which I consider fairly decent.

Simply Wallstreet

Above shows how revenues and earnings have been changing through the years. Revenues and earnings are projected to improve, and I'm confident the company will attain the projected figures given its ambitious investments.

Balance Sheet

Looking at the balance sheet, I am assured of its short-term financial health, with its current ratio at 5.59. This means that Impinj can service its current liabilities with its existing assets by about 5.59x. On top of that, the cash available at $ 154.5 million can cover the MRQ's operating expenses ($ 48 million) by about 3.2x. This gives investors confidence in its ability to cover its short-run financial obligations.

Considering the company's long-term financial health, its total debt amounts to $ 293.9 million. It has a total equity of $ 26.6 million, bringing its debt-to-equity ratio to 1104.8%, which is quite high. Considering the cash balance, its net debt of $ 139.4 million is also high, an indication of a highly leveraged balance sheet. Impinj has not been profitable over the last few years as it has been recording negative earnings. The company cannot cover its interest expenses at $ 4.9 million with a negative EBIT.

Despite the gloomy debt ratios, the cash available can cover the MRQ's operating expenses ($48million) by about 3.2x. On top of that, although it has significantly high debt and net debt-to-equity ratios, it is important to note that the debt matures in 2027. With this reasonable time frame, the company can address its financial obligations and improve its financial position.

What's New?

The company recently acquired a Finnish company, Voyantic; a market leader providing test and measurement solutions for designing and manufacturing RFID inlays and labels. These solutions serve inlay and label manufacturers, service bureaus, technology vendors, and consumers. The acquisition will broaden the portfolio of solutions offered by Impinj and enhance the leading position of its platform in terms of RAIN RFID quality, readability, and reliability.

Risks

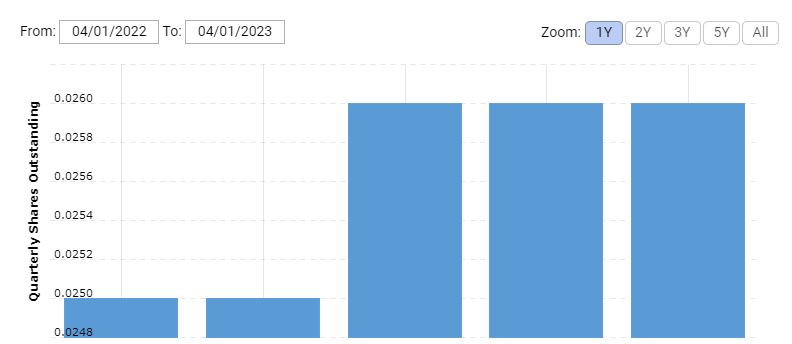

Impinj has a significant debt with debt and net debt to equity ratios of 1104.1% and 524%, which is significantly high. Further, the company has reported negative cash flows TTM, which is inadequate to service its debt. With its negative earnings, neither can it cover its interest payments. PI has also been reporting losses over the past few years. It also issued new shares during the previous year, increasing its total outstanding by about 5.2%.

Macrotrends

The increase in outstanding shares shows that shareholders have been diluted, thus decreasing their existing ownership percentage.

Conclusion

PI offers RAIN RFID solutions to its global customers. It has expanded the capabilities of the RFID chips and used the opportunity to grow. Its strong demand has also been a plus in its growth journey. The company has registered decent revenues, and the revenues and earnings projections look promising. Since it recently acquired Voyantic, it can build and grow its leading position regarding RFID offerings. Despite risks, I am confident in the stock's performance and thus rate it a buy.

"though" - Google News

May 15, 2023 at 03:12PM

https://ift.tt/EAUGsqk

Impinj: Though Debt Ridden, There Are Reasons To Be Bullish (NASDAQ:PI) - Seeking Alpha

"though" - Google News

https://ift.tt/Pkj1u2W

https://ift.tt/sQHwIBi

Bagikan Berita Ini

0 Response to "Impinj: Though Debt Ridden, There Are Reasons To Be Bullish (NASDAQ:PI) - Seeking Alpha"

Post a Comment